What Is Chargeback Prevention? Essential Basics for Beginner Business Owners to Protect Profits

When operating an EC site, "protecting profits" is just as important as increasing sales. One of the biggest barriers to this is "chargebacks." A chargeback occurs when a credit card holder does not consent to a transaction for reasons such as fraudulent use, and the card company (issuer) forcibly reverses the sale — even if the product has already been shipped, the sales revenue is confiscated. In this article, we explain the definition of chargebacks and their countermeasures in an easy-to-understand manner for beginners.

Table of Contents (Click to Expand)

1. The Definition of Chargebacks and Their Financial Impact on EC Businesses

A chargeback occurs when a cardholder disputes a transaction and the payment processor reverses the charge. This means lost revenue plus fees of typically $20-$100 per incident.

Chargeback costs extend beyond the refunded amount: sellers face chargeback fees of $15-25 per incident, potential loss of payment processing privileges at 1%+ chargeback rates, and increased reserve requirements from payment processors.

2. Typical Patterns of Fraudulent Use and Risk Analysis

Three categories: fraud (unauthorized use), service issues (not as described), and friendly fraud (buyer remorse). Each requires different prevention strategies.

In recent years, a technique called "credit master" (card number validity testing) — where automated programs test thousands of card numbers in rapid succession — has been increasing. Sites without adequate security measures are targeted for this type of attack, and the resulting chargebacks can accumulate rapidly.

- Third-Party Impersonation: Fraudulent payments using stolen card information. Lists circulated on the dark web, etc., may be used.

- Cardholder Denial (Friendly Fraud): Cases where the cardholder makes a false claim of "no recollection" despite having made the purchase. This includes intentional abuse.

- Non-Delivery/Damage: Claims filed due to shipping issues. Evidence management is crucial.

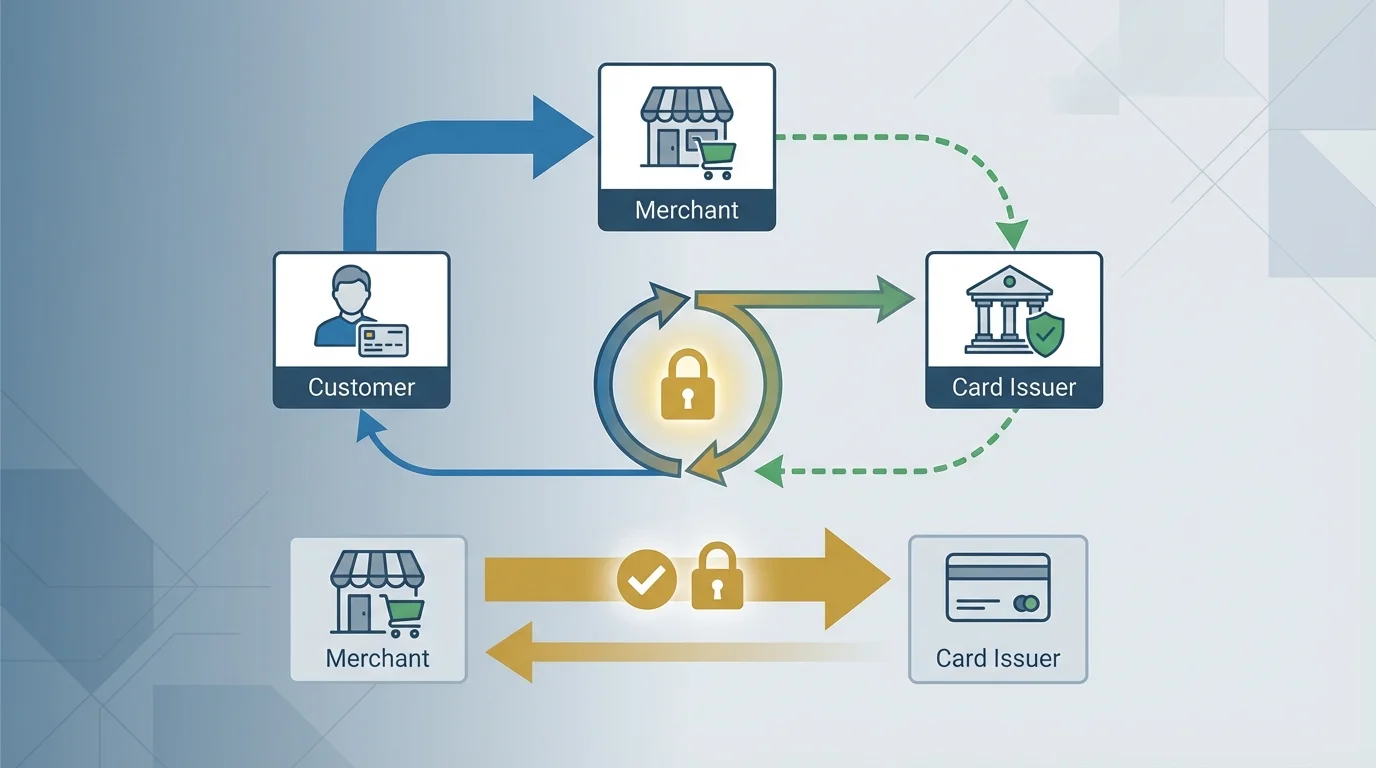

3. The Ultimate Defense: How "EMV 3-D Secure" Works

Build systems with: clear billing descriptors, proactive customer communication, delivery tracking, easy refund processes, 3D Secure authentication, and address verification.

Implementing 3D Secure authentication, Address Verification System (AVS), and CVV verification can reduce chargebacks by 40-60%. Additionally, clear billing descriptors help customers recognize charges and prevent friendly fraud.

4. The Current State of Unauthorized Access Seen Through Statistics

The following graph shows the percentage of "suspected fraudulent access" blocked by security filters among payment attempts on a typical EC site. Sites without countermeasures are more likely to see latent risks materialize.

Frequently Asked Questions

- Q. How should you handle a chargeback when it occurs?

- A. Respond promptly by gathering all transaction evidence. Submit compelling representment with clear documentation. Speed and thoroughness significantly impact reversal success.

- Q. What is the acceptable chargeback rate?

- A. Most processors flag accounts exceeding 1%. Maintaining below 0.5% is recommended. Prevention is far more cost-effective than dispute resolution.

Take Your EC Business to the Next Stage

From payment optimization to comprehensive EC risk management, our expert consultants provide data-driven solutions.

Get Free Strategy ConsultationSummary

Chargebacks are a significant profit threat. Understanding the three types, implementing comprehensive prevention, and establishing rapid response protocols are essential for protecting revenue and payment processor relationships.

Published: 2026-03-04 / Author: Yuta Ito

Related Articles

References

- [1] Payment Card Industry: Chargeback Management Guide

- [2] Visa/Mastercard Dispute Resolution Best Practices