[For Beginners] What Is Chargeback? Payment Risks Threatening EC Sites and the Necessity of 3D Secure 2.0

For EC site operators, more important than increasing sales is "ensuring reliable payment collection." However, an unavoidable risk when accepting credit card payments is"chargeback" risk — when cardholders dispute charges citing fraud, sales are forcibly reversed. This article covers chargeback basics through 3D Secure 2.0 benefits essential for 2025, explained both professionally and accessibly.

Table of Contents (Click to expand/collapse)

1. Chargeback Definition and Three Primary Causes

A chargeback is a mechanism where a cardholder disputes a charge for reasons like "unrecognized billing," and the card company reverses the sale. For EC operators, this means"products already shipped (inventory loss) but sales revenue unrecoverable (profit loss)" — a double punch of risk.

Main causes are categorized into these 3 points (MECE classification):

- Third-party fraud: Fraudulent orders using stolen card information.

- Cardholder Denial: When the actual orderer claims "not delivered" or "family used it without permission."

- Product Issues/Non-delivery: Payment refusal due to dissatisfaction or delivery issues.

2. The Terror of "Liability Shift" Borne by EC Operators

The rule of who bears losses when chargebacks occur is called "liability." Under traditional payment methods, fraud responsibility fundamentally fell onEC merchants (operators). This is the state before "liability shift" occurs.

However, with proper identity verification (3D Secure, etc.), fraud liability shifts to the card issuer. This transfer of responsibility from merchant to card company is called "liability shift" in financial terminology.

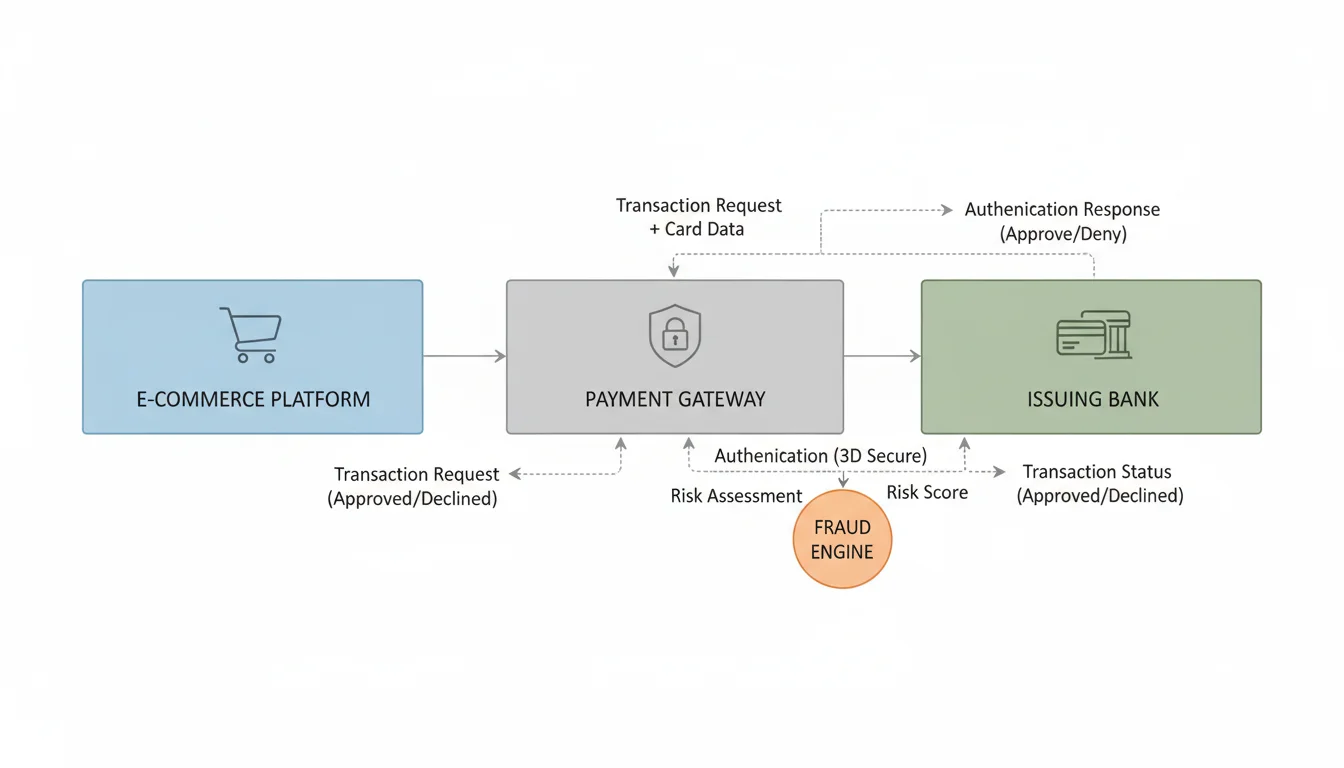

3. Defense Strategies Using 3D Secure 2.0 (EMV 3-D Secure)

Per METI guidelines, by March 2025, all EC merchants must implement3D Secure 2.0. Legacy 1.0 required mandatory passwords causing cart abandonment, but 2.0 adopts "Risk-Based Authentication."

This extracts only "suspicious transactions" from device info and purchase history, completing others without passwords — dramatically improving security without compromising UX.

4. Fraud Prevention Comparison Data

The chart below shows chargeback rate trends before and after 3D Secure implementation. Proper authentication minimizes fraud losses while maintaining healthy cash flow.

Frequently Asked Questions

- Q. If a chargeback occurs, will the product be returned?

- A. Unfortunately, in fraud cases products are usually already resold and rarely returned. Prevention measures are therefore extremely important.

- Q. Will 3D Secure 2.0 prevent 100% of losses?

- A. Liability shift means card companies bear financial losses from fraud. However, "merchant-caused" issues like product defects are excluded.

Take Your EC Business to the Next Stage

From payment risk reduction to CVR-maximizing UI/UX design, our professional consultants provide support.

Consult on Strategy for FreeSummary

Chargeback is an "invisible enemy" directly cutting EC site profits. However, implementing 3D Secure 2.0 and understanding liability shift significantly reduces risk. Don't wait for 2025 mandates — review your payment environment now for safe, sustainable EC operations.

Published: 2026-03-04

Read Also

References

- [1] METI "Strengthening Credit Card Payment Security Measures"

- [2] Japan Credit Association "Fraud Damage Statistics"